Equity investment at the corporate level involves a strategic partnership, where an investor commits to providing a developer with a total equity facility to invest in multiple schemes across several years, as a means to facilitate their growth strategy.

This approach can be attractive to developers due to the benefits these facilities provide. In this blog, we will review the advantages and disadvantages of raising equity at the corporate level and how this compares against raising equity on a scheme-by-scheme basis.

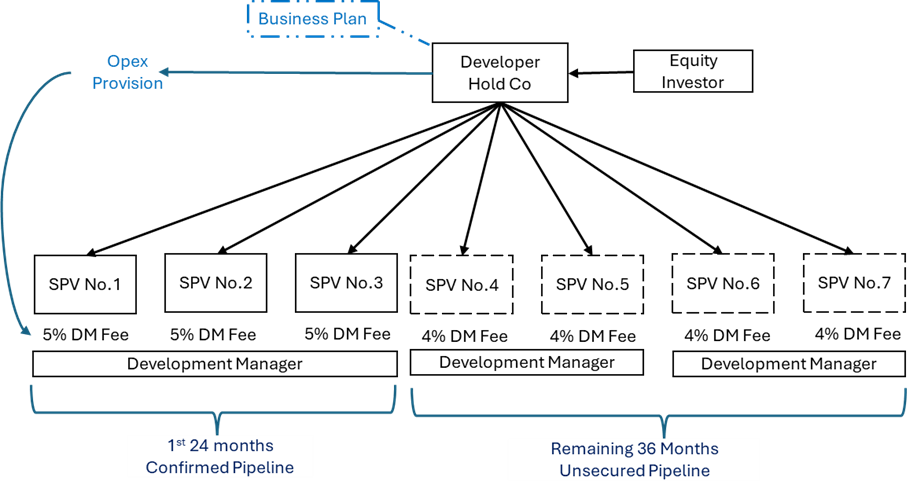

How corporate equity investment is structured

The main agreement of equity at the corporate level, as shown in the illustration below, is between an investor and developer’s main holding company. The foundation of these agreements is built on a developer’s business plan, which serves as the basis for negotiating key elements such as the total facility equity amount, duration, scheme criteria and agreement conditions.

Like raising equity for a single scheme, this can be either through pure equity or preferred equity. The main agreement will confirm the waterfall structure for repayment of any sales proceeds.

Securities in these agreements resemble those of an SPV shareholder agreement. In addition, investors will also require fixed charges over the borrower’s main holding company, assignment rights over all borrower loans, and collateral warranties for all schemes.

Where these facilities are typically up to five years, a developer might have a partially secured pipeline and need to find additional projects for the remainder of the equity agreement term.

A pre-defined framework will be in place confirming scheme criteria, with each new scheme subject to investor approval and due diligence. New SPVs and shareholder agreements will be established once approved, with a development manager fee provided for operating expenses.

The benefits of raising equity at the corporate Level

1. Streamlined process: securing a committed equity facility eliminates the requirement to tender equity from the market for each individual scheme, saving weeks on sourcing equity.

2. Strong purchasing position: developers with committed funds ready to deploy hold a much stronger buying position compared to those needing to source equity externally.

3. Improved negotiation power: developers with committed facilities have stronger negotiation power with stakeholders such as lenders, suppliers, and contractors, where these facilities signify a strong pipeline and potential opportunities for repeat business.

4. Reduced fees: upfront corporate agreements between investors and developers can carry expensive upfront costs, but they can save on overall reduced legal and arrangement fees, where each new scheme is drawn down as a new tranche of the main equity agreement.

5. Strategic partnership: corporate-level investment involves forging long-term partnerships with investors who are invested in the developer’s success, providing access to valuable expertise and networks to enhance future projects. Additionally, investors might have the ability to adapt in challenging markets, for example, adjusting scheme criteria to meet market trends e.g. change of use from a residential tower to student accommodation.

- The Finance Professional Show 2023: The Video

- Equity Masterclass: Structuring the capital stack, SPVs and shareholder agreements

- Equity Masterclass: a pivotal tool for development funding

6. Enterprise value: this approach can build the value of a developer’s business through improving their reputation; directly employing professionals; and establishing supply chains and land banks, which can be beneficial in the long term should a developer consider selling their business.

The downsides of raising equity at the corporate level

1. Developer eligibility: this type of equity investment is accessible only to experienced developers. Investors need strong track records when entering long-term partnerships.

2. Developer liquidity: these agreements can require the developer to put upfront capital into a blocked account for the purpose of the equity input into a new scheme, therefore sufficient liquidity and upfront commitment to these partnerships may be necessary.

3. Investor flexibility: where these facilities are in short supply, investors might exhibit less flexibility in negotiating the terms of an agreement.

4. Longer negotiation and upfront due diligence: as these partnerships span across several years, upfront negotiation, due diligence and relationship building processes can be slow.

5. Non-utilisation fees: undrawn capital is often subject to non-utilisation fees. Therefore, developers should secure a total equity facility based on what they will need.

6. Market dependence and volatility: developer success can be significantly influenced by market conditions. In a volatile market with limited opportunities, developers might feel the pressure of having to push on with less profitable schemes, through their committed facility.

7. Development manager fees: some agreements provide higher DM fees initially, such as 5% for the first 24 months, 4% for the subsequent 12 months, and 3% thereafter. Developers must cautiously manage their cashflow. Additional schemes might necessitate appointing more development managers, therefore impacting operating cashflow.

8. Profit realisation: corporate equity agreements might have restrictions on withdrawing profits until a certain number of schemes or profits have been completed. This means that developers might not have access to their well-earned profits immediately.

Conclusion: striking the balance between corporate vs single scheme equity

The decision between raising equity on a scheme-by-scheme basis and at the corporate level is not a one-size-fits-all proposition. Both approaches offer advantages and present unique challenges that developers must consider carefully.

Corporate-level equity investment can be an excellent tool for a developer’s growth through forming a strategic partnership with an equity investor. These facilities streamline processes, provide stronger purchasing power, reduce overall fees, and can enhance enterprise value. However, they also include pitfalls such as eligibility requirements, long agreement periods, market dependency, cashflow obligations, non-utilisation fees and profit-realisation restrictions.

On the other hand, raising equity on a single scheme offers flexibility, tailored structuring of the capital stack and less commitment. Nevertheless, this approach can involve higher transaction costs, can be much slower and more uncertain in securing funding for each new scheme.

In conclusion, the choice between raising corporate-level and single scheme equity investment should be subject to a developer’s position. One approach might be more suitable than another.

Developers should carefully consider both types of equity funding and ensure that they have strong legal counsel when entering into any agreements.

Leave a comment